In [1]:

from lec_utils import *

import lec20_util as util

Discussion Slides: Gradient Descent and Classification

Agenda 📆¶

- Gradient descent.

- Classification.

- Evaluating classification models.

Overview¶

- In order to find optimal model parameters, $w_0^*, w_1^*, ..., w_d^*$, our goal has been to minimize empirical risk.

- We've minimized empirical risk functions (like $R$ above) a few ways so far:

- Taking (partial) derivatives, setting them to 0, and solving.

- Using a linear algebraic-argument, which led to the normal equations, $X^TX \vec w^* = X^T \vec y$.

- Gradient descent is a method for minimizing functions computationally, when doing so by hand is difficult or impossible.

Gradient descent¶

- Suppose we want to minimize a function $f$, which takes in a vector $\vec w$ as input and returns a scalar as output.

For example, $f$ could be (but doesn't need to be) some empirical risk function, like the one on the previous slide.

To do so:

- Start with an initial guess of the minimizing input, $\vec w^{(0)}$.

- Choose a learning rate, or step size, $\alpha$.

- Use the following update rule:

$$\vec w^{(t+1)} = \vec w^{(t)} - \alpha \nabla f(\vec w^{(t)})$$

- $\nabla f(\vec{w}^{(t)})$ is the gradient of $f$, evaluated at timestep $t$.

The gradient of a function is a vector containing all of its partial derivatives.

- We repeat this iterative process until convergence, i.e. until the changes between $\vec{w}^{(t+1)}$ and $\vec{w}^{(t)}$ are small (or equivalently, until $\nabla f(\vec w^{(t)})$ is close to $\vec 0$.

In [2]:

util.minimizing_animation(w0=0, alpha=0.01)

Regression vs. classification¶

- So far in the course, we've been working with regression problems – where our goal is to predict some quantitative variable.

Examples: Predicting commute times, predicting house prices.

- With classification problems, our goal is to predict a categorical variable. These problems involve questions like:

- Is this email spam or not? This is an example of binary classification, in which we predict one of two possible classes..

- Is this picture of a dog, cat, zebra, or elephant? This is an example of multiclass classification, in which we predict one class from more than two possible options.

- We learned about two classification models in Wednesday's lecture: $k$-nearest neighbors and decision trees.

The most common evaluation metric in classification is accuracy:

$$\text{accuracy} = \frac{\text{# points classified correctly}}{\text{# points}}$$

Accuracy ranges from 0 to 1, i.e. 0% to 100%. Higher values indicate better model performance.

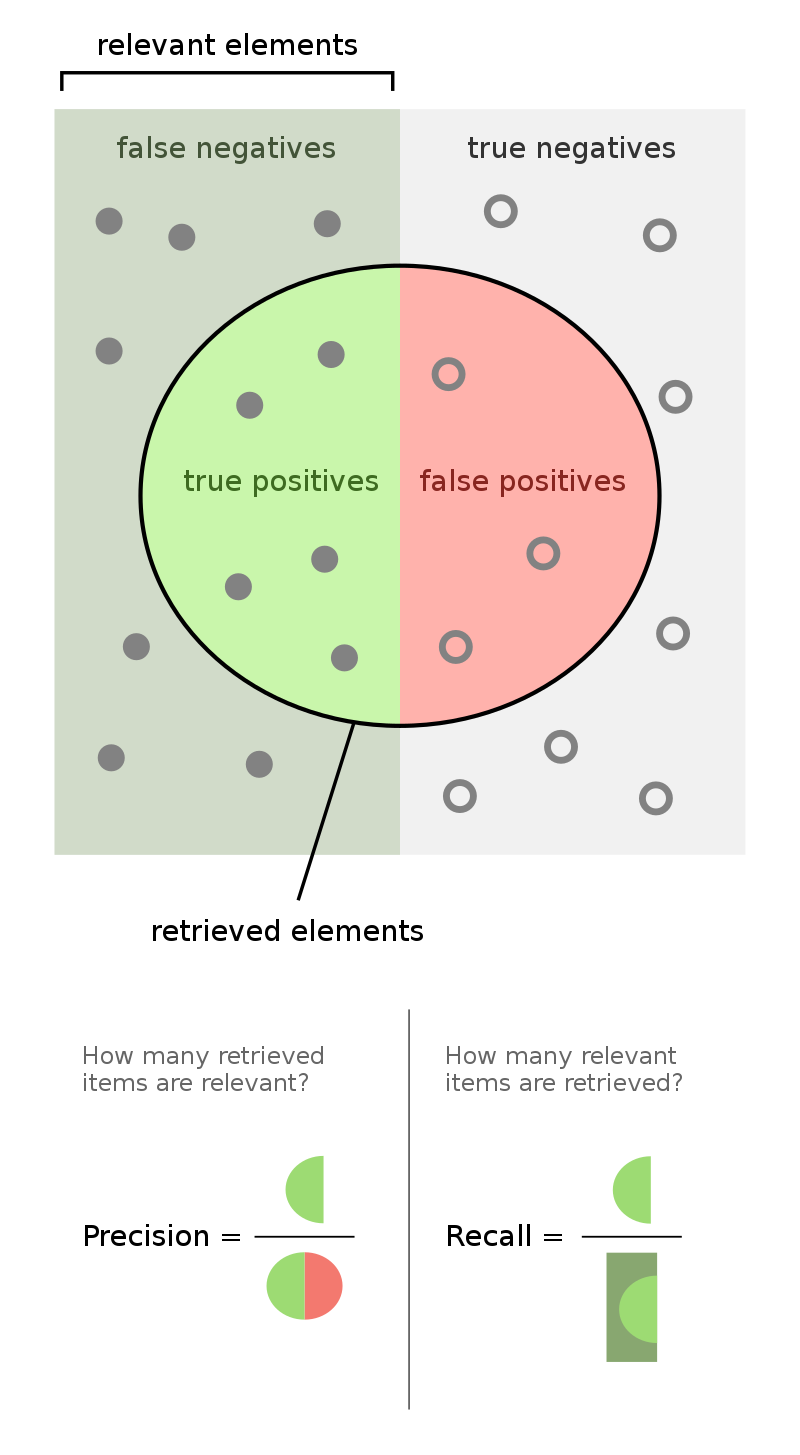

Evaluating classification models¶

- When we perform binary classification, there are 4 possible outcomes.

| Outcome of Prediction | Definition | True Class |

|---|---|---|

| True positive (TP) ✅ | The predictor correctly predicts the positive class. | P |

| False negative (FN) ❌ | The predictor incorrectly predicts the negative class. | P |

| True negative (TN) ✅ | The predictor correctly predicts the negative class. | N |

| False positive (FP) ❌ | The predictor incorrectly predicts the positive class. | N |

- We often evaluate classifiers using precision and recall.